The global semiconductor equipment market is experiencing robust expansion, driven by rising demand for advanced electronics, accelerated adoption of 5G, AI, and IoT technologies, and increased investments in semiconductor fabrication capacity. According to a 2023 report by Mordor Intelligence, the market was valued at USD 96.7 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 6.5% from 2023 to 2028, reaching an estimated USD 141.2 billion by 2028. This growth is further fueled by regional initiatives to strengthen domestic semiconductor supply chains, including the U.S. CHIPS and Science Act and similar programs in Europe and Asia. As the industry scales to meet demand for cutting-edge process nodes and next-generation chips, equipment manufacturers play a pivotal role in enabling innovation and production efficiency. The following list highlights the top 10 semiconductor equipment manufacturers leading this transformation, ranked based on market influence, revenue performance, and technological leadership.

Top 10 Semiconductor Equipment Manufacturers 2026

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Semiconductor Equipment

H2 2026 Market Trends Analysis: Semiconductor Equipment

As the global semiconductor industry approaches the second half of 2026 (H2 2026), the semiconductor equipment market is poised for continued evolution, driven by technological innovation, geopolitical dynamics, and shifting end-market demand. Below is a comprehensive analysis of the key trends shaping the semiconductor equipment landscape during this period.

1. Strong Demand from AI and HPC Driving Equipment Spending

Artificial Intelligence (AI) and High-Performance Computing (HPC) remain the primary growth engines for semiconductor equipment demand. By H2 2026, AI-specific chips—particularly GPUs, TPUs, and custom accelerators—require advanced process nodes (sub-3nm and 2nm) and complex packaging techniques such as chiplets and 3D stacking. This has led to sustained capital expenditure (capex) from hyperscalers and foundries, particularly TSMC, Samsung, and Intel.

- Equipment Implications: Increased demand for extreme ultraviolet (EUV) lithography tools (ASML), advanced etch (Lam Research), deposition (Applied Materials), and metrology tools.

- Trend: Adoption of High-NA EUV lithography is accelerating in H2 2026, with initial production ramps at leading-edge nodes.

2. Geopolitical Realignment and Regionalization of Supply Chains

Geopolitical tensions—particularly between the U.S., China, and Taiwan—continue to influence equipment procurement and manufacturing strategies.

- U.S. and EU Investment: CHIPS Act funding in the U.S. and the EU Chips Act are driving localization of semiconductor manufacturing. By H2 2026, new fabrication plants (fabs) in Arizona, Ohio, and Germany are entering volume production, boosting demand for front-end equipment.

- China’s Self-Reliance Push: Despite export controls, China is investing heavily in domestic equipment capabilities. Chinese suppliers (e.g., SMEE, NAURA, AMEC) are gaining traction in mature nodes (<28nm), supporting growth in local equipment markets.

- Trend: Dual supply chains are emerging—one for advanced nodes (dominated by U.S., EU, and allied nations) and one for mature nodes (with increasing Chinese autonomy).

3. Mature Node Equipment Demand Remains Robust

While much attention is focused on cutting-edge nodes, mature and specialty process nodes (40nm and above) continue to drive significant equipment demand in H2 2026.

- Applications: Automotive, industrial IoT, power management, and consumer electronics require stable, cost-effective manufacturing.

- Equipment Impact: Strong demand for legacy lithography (DUV), wet processing, and backend assembly tools.

- Trend: Equipment vendors are optimizing tools for cost efficiency and throughput in mature fabs, supporting long-term capacity expansion in Southeast Asia and India.

4. Advanced Packaging as a Key Growth Vector

With Moore’s Law slowing, advanced packaging technologies (e.g., CoWoS, Foveros, FOPLP) are critical for performance gains. TSMC, Intel, and Samsung are expanding advanced packaging capacity.

- H2 2026 Developments: Increased capex in fan-out wafer-level packaging (FOWLP), hybrid bonding, and silicon interposers.

- Equipment Demand: Surge in tools for temporary bonding, thin-wafer handling, bumping, and inspection.

- Trend: Equipment vendors are forming strategic partnerships with OSATs (outsourced semiconductor assembly and test) and IDMs to co-develop packaging solutions.

5. Sustainability and Equipment Efficiency Gains

Environmental, Social, and Governance (ESG) pressures are pushing fabs to reduce energy and water consumption. Equipment manufacturers are responding with more sustainable tools.

- H2 2026 Innovations:

- Energy-efficient plasma etch and CVD systems.

- Closed-loop chemical recycling in wet stations.

- AI-driven predictive maintenance to reduce tool downtime and waste.

- Trend: Green manufacturing is becoming a competitive differentiator, with leading equipment firms disclosing carbon footprints and offering lifecycle management services.

6. Consolidation and Strategic Partnerships in Equipment Ecosystem

The high cost of R&D for next-generation tools is driving consolidation and collaboration.

- M&A Activity: Mid-tier equipment firms are being acquired by larger players to expand technology portfolios (e.g., in metrology, defect inspection).

- Joint Development: Foundries and equipment vendors are co-developing tools tailored to specific process requirements (e.g., gate-all-around transistor integration).

- Trend: Vertical integration and ecosystem partnerships are becoming essential for maintaining technological leadership.

7. Market Outlook and Financial Performance

By H2 2026, the semiconductor equipment market is projected to grow at a CAGR of ~8–10% year-over-year, reaching an estimated $130–140 billion annually.

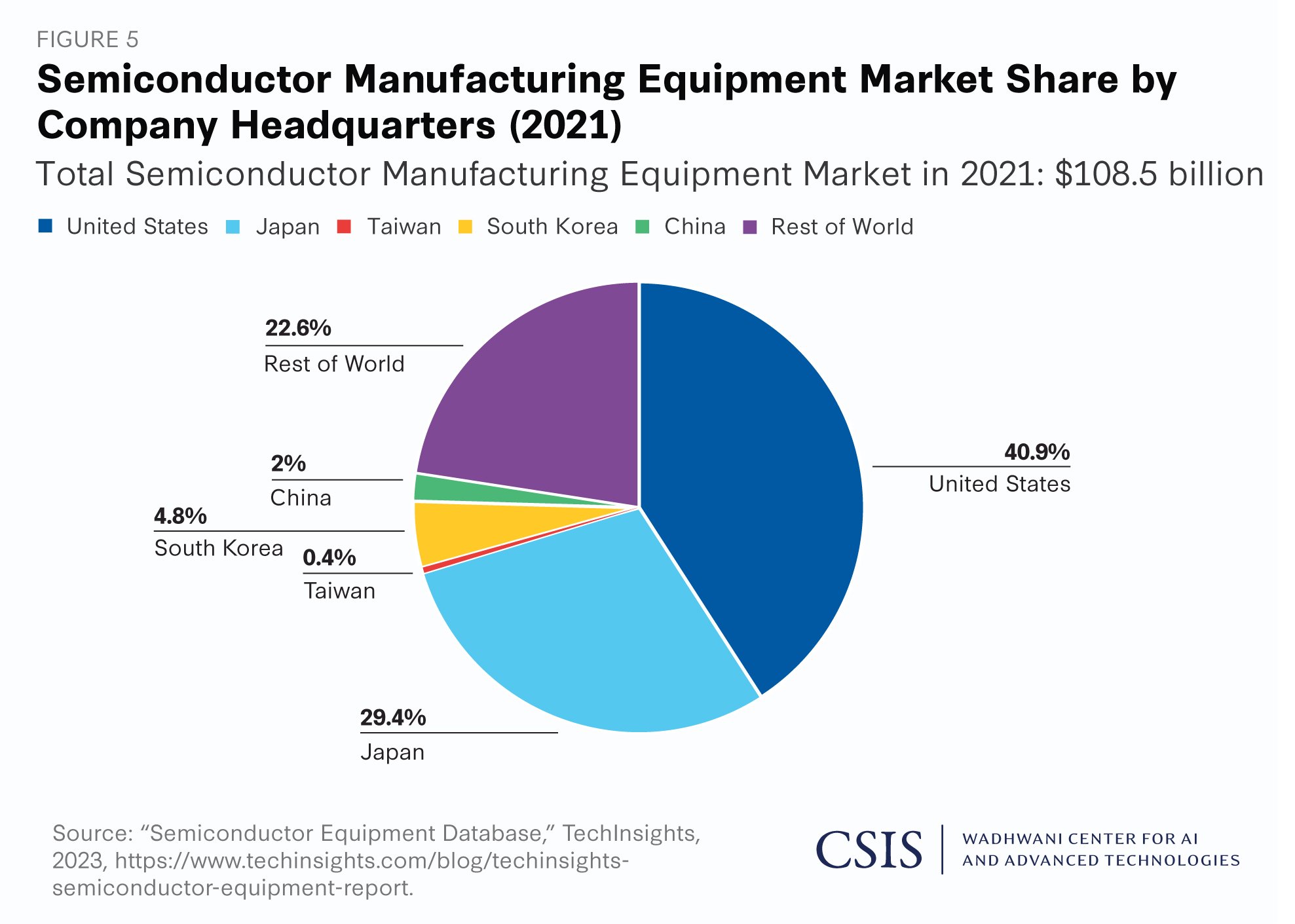

- Regional Breakdown:

- Asia-Pacific (ex-China): ~45%

- China: ~20% (driven by mature nodes and government support)

- North America: ~20% (new fab ramps)

- Europe: ~10%

- Key Players: ASML, Applied Materials, Lam Research, Tokyo Electron, and KLA remain dominant, with growing influence from Chinese equipment firms in domestic markets.

Conclusion

H2 2026 marks a pivotal phase in the semiconductor equipment industry, characterized by technological bifurcation (advanced vs. mature nodes), geopolitical fragmentation, and increased focus on sustainability and packaging. Equipment vendors that can navigate export controls, innovate rapidly, and support diverse manufacturing ecosystems will be best positioned for long-term success. The market remains robust, underpinned by structural demand from AI, automotive electrification, and digital infrastructure.

Common Pitfalls Sourcing Semiconductor Equipment: Quality and Intellectual Property Risks

Sourcing semiconductor equipment involves significant technical, financial, and legal complexities. Two of the most critical areas where organizations encounter pitfalls are quality assurance and intellectual property (IP) protection. Overlooking these aspects can lead to production delays, yield issues, legal liabilities, and loss of competitive advantage.

Quality-Related Pitfalls

-

Inadequate Supplier Vetting and Qualification

Failing to conduct thorough due diligence on equipment suppliers—especially new or lower-cost vendors—can result in unreliable equipment. This includes overlooking a supplier’s track record, manufacturing capabilities, adherence to industry standards (e.g., SEMI), and quality management systems (e.g., ISO 9001). -

Lack of Clear Equipment Specifications and Acceptance Criteria

Vague or incomplete technical specifications increase the risk of receiving equipment that does not meet process requirements. Without defined performance metrics, uptime expectations, or process integration standards, quality disputes become common during installation and qualification. -

Insufficient Factory Acceptance Testing (FAT) and Site Acceptance Testing (SAT)

Skipping or inadequately executing FAT and SAT procedures can allow defects to go unnoticed until the equipment is installed in the cleanroom. This leads to costly rework, schedule delays, and potential contamination risks. -

Poor Documentation and Traceability

Equipment lacking complete documentation—such as maintenance logs, calibration records, spare parts lists, and as-built schematics—compromises long-term reliability and maintenance. This is particularly problematic for refurbished or second-hand systems. -

Overlooking Component-Level Quality and Supply Chain Transparency

Semiconductor tools depend on high-precision components (e.g., sensors, pumps, robotics). Sourcing equipment without visibility into the origin and quality of subcomponents risks vulnerabilities such as counterfeit parts, obsolescence, or reliance on restricted suppliers.

Intellectual Property-Related Pitfalls

-

Ambiguous Ownership of Customizations and Process Know-How

When equipment is customized for a specific manufacturing process, unclear contractual terms can leave ownership of modifications, software, or process data in dispute. This risks losing control over proprietary process IP developed during equipment integration. -

Inadequate Protection of Trade Secrets During Evaluation and Integration

Sharing sensitive process parameters, yield data, or fab layouts with suppliers during testing or support exposes critical IP. Without robust non-disclosure agreements (NDAs) and data access controls, this information may be inadvertently or deliberately exploited. -

Hidden or Undisclosed Third-Party IP in Equipment Software and Firmware

Equipment often includes embedded software with licensed third-party code. Sourcing without IP audits or warranties can expose the buyer to infringement claims, especially if open-source licenses (e.g., GPL) impose unintended distribution obligations. -

Failure to Secure License Rights for Software and Upgrades

Some suppliers restrict the use, modification, or transfer of control software. Without explicit licensing terms, companies may face limitations in maintaining, upgrading, or transferring equipment—particularly during fab expansions or M&A activities. -

Reuse of Equipment with Embedded IP from Previous Owners

When purchasing used or refurbished tools, residual software, calibration data, or configurations from prior users may contain proprietary information. Failure to properly sanitize or audit such equipment risks IP contamination and compliance issues.

To mitigate these risks, organizations should implement rigorous procurement protocols, engage cross-functional teams (engineering, legal, IP counsel), and ensure contracts include clear quality standards, IP ownership clauses, audit rights, and compliance requirements.

Logistics & Compliance Guide for Semiconductor Equipment

Overview

Semiconductor equipment encompasses highly specialized, sensitive manufacturing tools used in the production of integrated circuits. Due to their technical complexity, high value, and strategic importance, the logistics and compliance requirements for moving such equipment—whether new, used, refurbished, or for repair—are significantly more stringent than for general industrial goods. This guide outlines key considerations for global transportation, regulatory compliance, and supply chain best practices.

Export Controls & Trade Compliance

Semiconductor manufacturing equipment is subject to strict export control regulations due to its dual-use potential and national security implications.

- ITAR and EAR Compliance: Most semiconductor equipment falls under the Export Administration Regulations (EAR), specifically controlled under the Commerce Control List (CCL) with Export Control Classification Numbers (ECCNs) such as 3B001, 3B002, and 2B350. Certain specialized tools may also trigger International Traffic in Arms Regulations (ITAR) controls if they meet military-grade specifications.

- Licensing Requirements: Shipments to certain destinations (e.g., China, Russia, Iran) often require export licenses from the U.S. Department of Commerce (BIS) or other national authorities. License exceptions (e.g., TMP, RPL) may apply but must be carefully evaluated.

- Deemed Exports: Technical data or assistance provided to foreign nationals within a domestic facility may constitute a “deemed export” and require authorization.

Packaging & Handling

Semiconductor tools are precision instruments, often sensitive to vibration, static discharge, moisture, and particulate contamination.

- Custom Crating: Use shock-absorbing, climate-controlled, and anti-static packaging. Crates should meet ISPM 15 standards for international wood packaging.

- Cleanroom Handling: If equipment is cleanroom-rated, maintain contamination controls during loading/unloading using ESD-safe garments and tools.

- Orientation & Securing: Clearly mark “This Side Up” and secure internal components to prevent movement. Use tilt and shock sensors during transit.

Transportation & Shipping

Global movement requires coordination among air, sea, and ground logistics with precise route planning.

- Air Freight: Preferred for high-value, time-sensitive shipments. Requires oversized cargo handling and advance coordination with airlines.

- Ocean Freight: Used for large tools or bulk shipments. Requires special stowage (flat racks, open-top containers) and climate control for sensitive modules.

- Last-Mile Delivery: Final transport to the fab must involve clean trailers, trained handlers, and coordination with facility engineers for controlled entry.

Import Regulations & Customs Clearance

Each destination country imposes specific import controls and documentation requirements.

- Duty & Tariff Classification: Use accurate HS codes (e.g., 8486.20 for semiconductor manufacturing machines) to determine duty rates. Leverage preferential trade agreements where applicable.

- Local Compliance: Countries like China, South Korea, and the EU require additional certifications (e.g., CCC, KC, CE) for equipment operation and safety.

- Temporary Imports: For equipment undergoing repair or calibration, use temporary admission programs (e.g., ATA Carnet, U.S. Temporary Importation Under Bond) to defer duties.

Environmental, Health & Safety (EHS) Compliance

Semiconductor tools may contain hazardous materials or require special decommissioning.

- Hazardous Components: Identify and document presence of vacuum pumps, coolants, or compressed gases. Comply with IATA/IMDG regulations for dangerous goods if applicable.

- Decommissioning & Decontamination: Follow OEM procedures to safely remove process chemicals and purge systems before shipping. Maintain decontamination certificates.

- WEEE & RoHS: For equipment disposal or recycling, comply with Waste Electrical and Electronic Equipment (WEEE) and Restriction of Hazardous Substances (RoHS) directives in relevant jurisdictions.

Documentation & Recordkeeping

Accurate and complete documentation is critical for compliance and traceability.

- Required Documents: Commercial invoice, packing list, bill of lading/air waybill, export license (if applicable), ECCN classification, certificate of origin, and decontamination report.

- Audit Trail: Maintain records for at least five years to support compliance audits by customs or regulatory agencies.

Risk Management & Insurance

Given the high value and sensitivity of semiconductor equipment, comprehensive risk mitigation is essential.

- Specialized Insurance: Obtain all-risk cargo insurance covering transport, handling, and customs delays. Specify replacement value and include coverage for ESD or calibration damage.

- Contingency Planning: Develop response plans for delays, customs holds, or damage, including access to local technical support and spare parts.

Best Practices Summary

- Conduct pre-shipment compliance reviews for every movement.

- Partner with logistics providers experienced in high-tech industrial equipment.

- Train personnel on export controls, EHS protocols, and handling procedures.

- Leverage digital tracking and monitoring (GPS, temperature, shock) for real-time visibility.

- Maintain close coordination with OEMs, freight forwarders, and customs brokers.

Adhering to this guide ensures compliant, secure, and efficient movement of semiconductor equipment across global supply chains while minimizing regulatory, financial, and operational risks.

Conclusion: Sourcing Semiconductor Equipment Supplier

In conclusion, the selection of a semiconductor equipment supplier is a critical strategic decision that significantly impacts manufacturing efficiency, product quality, yield, and long-term competitiveness in the semiconductor industry. After thorough evaluation of technical capabilities, financial stability, global support infrastructure, compliance with industry standards, and innovation roadmap, it is evident that partnering with a reliable, technologically advanced, and service-oriented supplier is essential.

The chosen supplier demonstrates strong alignment with our production requirements, offering cutting-edge equipment with high precision, scalability, and integration capabilities necessary for advanced process nodes. Additionally, their proven track record, responsive technical support, and commitment to continuous improvement provide confidence in long-term partnership sustainability.

Moving forward, establishing clear communication channels, performance metrics, and collaboration frameworks will be key to ensuring seamless integration and ongoing optimization. By securing a capable and future-ready equipment supplier, we position ourselves to enhance manufacturing excellence, reduce time-to-market, and maintain a competitive edge in the rapidly evolving semiconductor landscape.