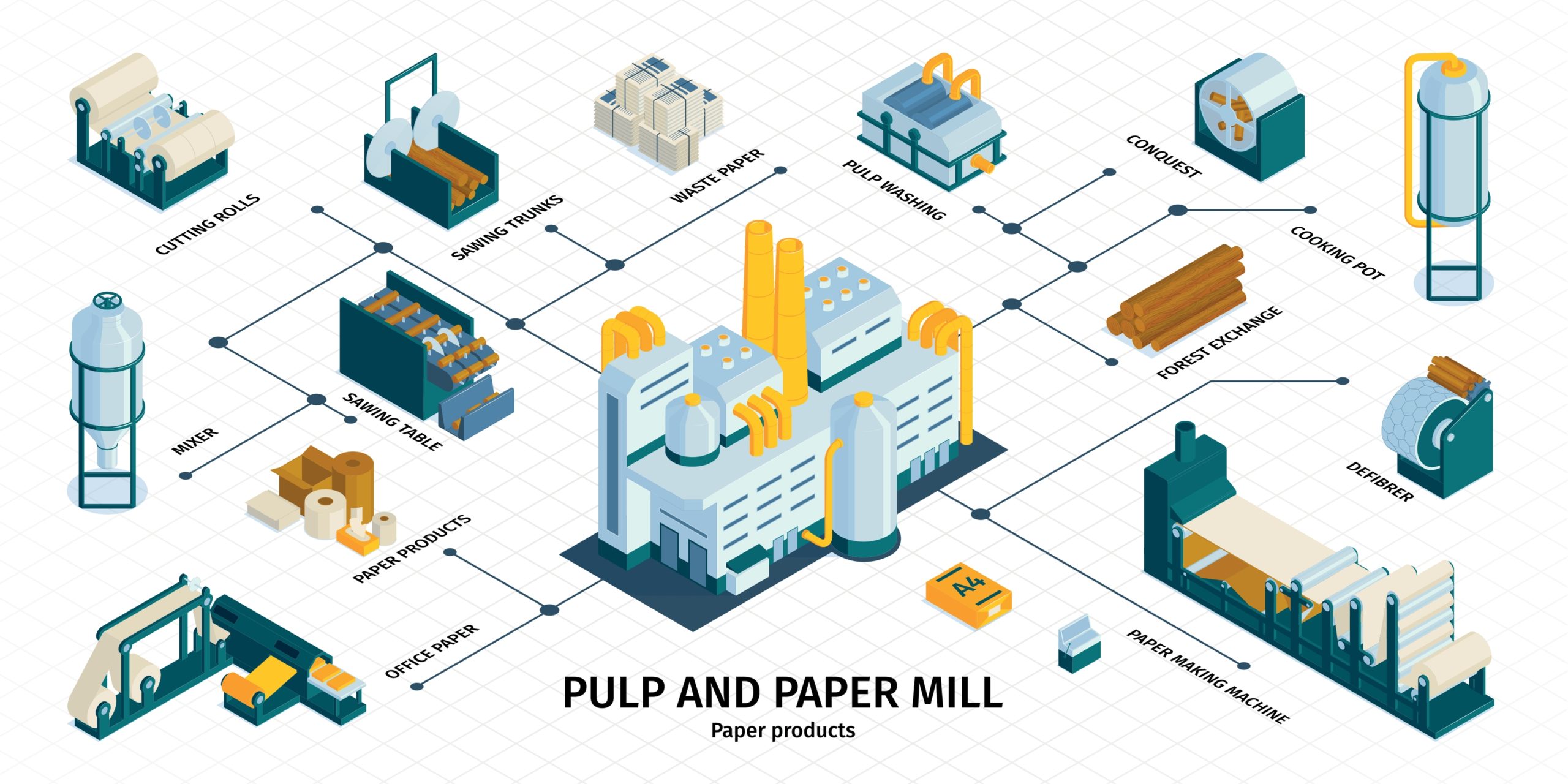

The global paper manufacturing industry continues to demonstrate resilience and steady growth despite the ongoing digital transformation across sectors. According to a 2023 report by Mordor Intelligence, the global paper market was valued at approximately USD 380 billion and is projected to grow at a CAGR of over 3.0% from 2023 to 2028. This growth is driven by sustained demand for packaging materials—particularly e-commerce packaging—and hygiene products such as tissue paper and paper towels. Similarly, Grand View Research estimates that the packaging segment alone accounted for more than 35% of total paper demand in 2022, with Asia-Pacific emerging as both the largest producer and consumer of paper due to rising industrialization and consumer spending.

Technological advancements, increasing emphasis on sustainability, and the adoption of recycled fibers are further reshaping the competitive landscape. In this evolving market, leading manufacturers are investing in efficient production processes, circular economy models, and green certifications to meet regulatory standards and consumer expectations. As demand shifts toward specialty and eco-friendly paper products, the following ten companies have emerged as industry leaders—based on production capacity, market reach, innovation, and revenue—shaping the future of the global paper industry.

Top 10 Paper Manufacturers 2026

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Paper

H2 2026 Market Trends for the Paper Industry

As the global economy evolves in 2026, the paper industry is navigating a complex landscape shaped by sustainability mandates, digital competition, shifting consumer behaviors, and technological innovation. The second half of 2026 is expected to solidify several key trends, leading to a more resilient yet transformed sector.

1. Accelerated Shift Toward Sustainable and Circular Models

Sustainability remains the dominant driver in H2 2026. Regulators, especially in the EU and North America, are enforcing stricter environmental standards, including extended producer responsibility (EPR) and deforestation-free supply chain requirements. As a result, paper producers are aggressively investing in:

– Recycled fiber integration, with many mills targeting over 80% recycled content for packaging grades.

– Certified virgin fiber sourcing (FSC/PEFC), particularly for premium and specialty papers.

– Carbon footprint reduction via renewable energy adoption, biomass boilers, and process optimization.

– Water stewardship and closed-loop systems to meet ESG reporting demands from investors and clients.

The “circular economy” is no longer a buzzword but a core operational strategy, with major players forming partnerships with waste management companies to secure reliable recycled fiber streams.

2. Packaging Dominance Amid E-Commerce Growth

The demand for paper-based packaging continues to outpace other paper segments. H2 2026 sees sustained growth driven by:

– E-commerce expansion, fueling demand for corrugated boxes, protective wraps, and lightweight shipping materials.

– Plastic substitution initiatives, as brands comply with single-use plastic bans and consumer preferences for recyclable materials.

– Innovation in functional packaging, including water-resistant coatings derived from bio-based materials and improved barrier technologies for food-grade papers.

Corrugated and containerboard remain the strongest performers, while specialty packaging (e.g., molded fiber, paper pouches) gains traction in food and cosmetics.

3. Continued Decline in Graphic Papers, Offset by Niche Print Demand

Traditional printing and writing paper markets remain under structural pressure due to digitalization. However, H2 2026 reveals stabilization in select segments:

– High-quality, specialty printing papers (e.g., for luxury packaging, art books, certificates) see modest growth driven by premiumization and tactile consumer experiences.

– Educational and institutional demand in emerging markets provides a buffer, though digitization efforts are progressing.

– Digital print compatibility has become essential, with mills adapting surfaces and coatings for inkjet and toner adhesion.

Overall, graphic paper production is expected to decline slightly but at a slower rate than in prior years, as efficiency gains and market consolidation support profitability.

4. Regional Divergence and Supply Chain Resilience

Geographic trends are increasingly influential:

– Asia-Pacific remains the growth engine, particularly China and India, driven by urbanization, rising middle-class consumption, and e-commerce. However, Chinese overcapacity continues to weigh on global prices.

– North America and Europe focus on high-value, sustainable products and import substitution to reduce reliance on volatile global supply chains. Nearshoring of packaging production is accelerating.

– Latin America and Africa show emerging opportunities in both packaging and tissue, supported by population growth and infrastructure development.

Supply chain resilience is a top priority, with companies diversifying fiber sourcing, investing in regional production hubs, and leveraging AI-driven logistics to mitigate disruptions.

5. Technological Integration and Industry Consolidation

H2 2026 marks deeper digital transformation:

– AI and IoT are widely adopted for predictive maintenance, energy optimization, and quality control in paper mills.

– Blockchain enhances traceability in fiber sourcing, improving transparency for sustainability claims.

– Automation reduces labor costs and improves consistency, particularly in converting and packaging operations.

Meanwhile, industry consolidation continues as smaller players struggle with capital demands for sustainability upgrades. Mergers and acquisitions focus on vertical integration (e.g., packaging converters acquiring mills) and geographic expansion.

Conclusion

By H2 2026, the paper industry is no longer defined by volume but by value, sustainability, and adaptability. While challenges persist—particularly in balancing recycled fiber supply with quality demands and managing energy costs—the sector is positioned for long-term resilience. Success hinges on innovation in circular models, strategic regional focus, and deep integration of digital technologies, ensuring paper remains a vital, evolving material in the global economy.

Common Pitfalls When Sourcing Paper (Quality, IP)

Sourcing paper for manufacturing, packaging, or printing projects involves more than just cost and availability. Overlooking key quality and intellectual property (IP) considerations can lead to production delays, customer dissatisfaction, or legal complications. Below are common pitfalls to avoid:

Inadequate Quality Specifications

One major pitfall is failing to define clear and comprehensive quality standards. Buyers may assume standard grades are sufficient, but variations in brightness, thickness, texture, and moisture content can significantly impact the final product. Without precise specifications, suppliers might deliver paper that meets minimum industry standards but fails to perform in your specific application.

Inconsistent Batch-to-Batch Quality

Even with defined specifications, inconsistent quality between production batches can occur—especially when sourcing from large or global suppliers. Variations in raw materials, manufacturing processes, or quality control procedures may result in noticeable differences in color, strength, or printability. This inconsistency can damage brand reputation, particularly in high-end printing or retail packaging.

Overlooking Environmental and Regulatory Compliance

Paper sourcing often involves sustainability claims such as FSC or PEFC certification. Misrepresenting or failing to verify these certifications not only undermines corporate social responsibility goals but may violate regulations or customer requirements. Additionally, some regions restrict certain inks, coatings, or recycled content levels, and non-compliance can result in shipment rejections.

Intellectual Property Risks in Custom Paper Designs

When sourcing custom-designed paper—such as branded textures, watermarking, or security features—failing to secure IP rights is a significant risk. Suppliers may claim ownership of design modifications or reuse proprietary patterns for other clients unless contracts explicitly assign IP to the buyer. This can lead to infringement issues or loss of competitive advantage.

Unprotected Specifications and Trade Secrets

Sharing detailed technical specifications, coating formulas, or finishing requirements with multiple suppliers increases the risk of trade secret exposure. Without robust non-disclosure agreements (NDAs) and controlled information sharing, sensitive data could be leaked or replicated by competitors.

Supplier Ownership of Tooling and Dies

For custom paper products requiring specific molds, dies, or embossing plates, suppliers may retain ownership of these assets. This limits flexibility and creates dependency, as switching suppliers could involve costly retooling. Always clarify tooling ownership in contracts to maintain control and protect long-term sourcing strategies.

Failure to Audit Supply Chain Transparency

Paper supply chains can be complex, involving multiple tiers of suppliers. Without auditing the full chain, companies risk indirect association with unethical practices such as illegal deforestation or labor violations. This not only affects brand image but may also trigger regulatory penalties under due diligence laws in the EU or elsewhere.

By addressing these pitfalls proactively—through rigorous specifications, strong contracts, IP protections, and supply chain due diligence—organizations can ensure reliable, compliant, and secure paper sourcing.

Logistics & Compliance Guide for Paper

This guide outlines key considerations for the logistics and regulatory compliance involved in the transportation, handling, and trade of paper products, including printing paper, packaging materials, tissue paper, and industrial paper rolls.

Transportation and Handling

Proper handling and transportation are essential to maintain paper quality and prevent damage during transit.

- Packaging: Paper must be securely wrapped in moisture-resistant materials (e.g., kraft paper, plastic film) and palletized to prevent shifting. Use edge protectors and corner boards for large rolls or stacks.

- Moisture Protection: Paper is highly sensitive to humidity and water. Ensure vehicles are dry and weather-tight. Avoid open trucks in rainy or humid conditions.

- Temperature Control: Store and transport paper in climate-controlled environments when possible to prevent warping or curling, especially for high-quality printing paper.

- Stacking and Weight Distribution: Do not exceed weight limits on pallets or vehicles. Stack paper evenly to prevent collapse or deformation. Rolls should be transported on their sides and secured to prevent rolling.

- Forklift Safety: Use appropriate slings or roll clamps for paper rolls. Avoid puncturing or crushing paper bundles during loading/unloading.

Storage Requirements

Appropriate storage conditions help preserve paper quality and safety.

- Dry Environment: Store paper in clean, dry warehouses with relative humidity between 40–60% and temperatures between 15–25°C (59–77°F).

- Ventilation: Ensure adequate airflow to prevent mold and mildew development.

- Pallet Storage: Keep paper off the floor using wooden or plastic pallets. Avoid direct contact with concrete.

- Fire Safety: Paper is combustible. Store away from ignition sources and comply with local fire codes, including proper fire extinguisher placement and sprinkler systems.

Regulatory Compliance

Paper logistics must adhere to various international, national, and regional regulations.

- Customs Documentation: For cross-border shipments, ensure accurate commercial invoices, packing lists, and certificates of origin. Harmonized System (HS) codes for paper vary by type (e.g., 4802 for uncoated paper, 4819 for paper packaging).

- REACH and SVHC Compliance (EU): Paper products intended for consumer use must comply with REACH regulations, particularly regarding Substances of Very High Concern (SVHCs) in coatings or inks.

- FDA Regulations (USA): Paper intended for food contact (e.g., food packaging, paper towels) must comply with FDA 21 CFR regulations on food-safe materials and migration limits.

- FSC and PEFC Certification: If marketing paper as sustainably sourced, maintain valid chain-of-custody documentation from recognized bodies like FSC (Forest Stewardship Council) or PEFC (Programme for the Endorsement of Forest Certification).

- Import/Export Restrictions: Some countries restrict or tax paper imports based on environmental policies or trade agreements. Verify requirements with local customs authorities.

Environmental and Sustainability Considerations

Sustainable practices are increasingly important in paper logistics.

- Recycled Content: Clearly label and document the percentage of recycled fiber in paper products, especially when required by regulation or customer demand.

- Waste Management: Follow local regulations for disposing of damaged or contaminated paper. Recycle whenever possible.

- Carbon Footprint: Optimize transportation routes and use fuel-efficient vehicles to reduce emissions. Consider carbon offset programs for long-distance shipments.

Safety and Labeling

Ensure worker safety and regulatory adherence through proper labeling and procedures.

- Hazard Communication: While most paper is non-hazardous, coated or chemically treated paper may require Safety Data Sheets (SDS) under GHS regulations.

- Labeling: Clearly label packages with contents, weight, handling instructions (e.g., “This Way Up,” “Protect from Moisture”), and any relevant certifications (e.g., FSC, recyclable).

- Worker Training: Train warehouse and logistics personnel on safe handling techniques, emergency procedures, and proper use of protective equipment.

By following this guide, businesses can ensure efficient, compliant, and sustainable logistics operations for paper products across the supply chain.

Conclusion:

After a thorough evaluation of potential paper suppliers, including assessments of product quality, pricing, sustainability practices, delivery reliability, and customer service, [Supplier Name] emerges as the most suitable partner for our paper sourcing needs. Their consistent product quality, competitive pricing structure, commitment to environmentally responsible sourcing, and proven track record of on-time delivery align closely with our company’s operational and sustainability goals.

Additionally, [Supplier Name]’s ability to scale supply in response to demand fluctuations and their responsive customer support provide added assurance of a reliable long-term partnership. By selecting this supplier, we position our organization to maintain high product standards while supporting cost-efficiency and environmental responsibility across our supply chain.

We recommend moving forward with [Supplier Name] as our primary paper supplier, with a formal agreement to be established following final contract review. Regular performance evaluations will be conducted to ensure continued alignment with our quality and service expectations.