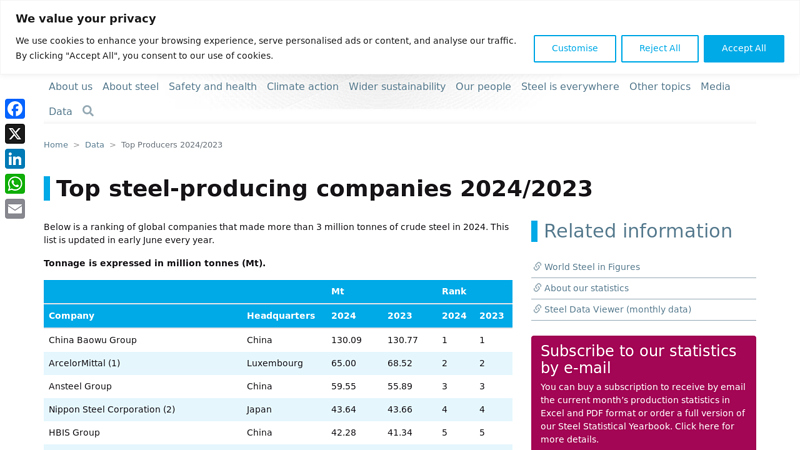

The global steel market, valued at approximately USD 1.2 trillion in 2023, is projected to grow at a compound annual growth rate (CAGR) of around 4.5% from 2024 to 2030, according to Grand View Research. This expansion is driven by rising infrastructure investments, increasing urbanization, and robust demand from construction, automotive, and manufacturing sectors—particularly in Asia-Pacific. As the backbone of industrial development, steel production is highly concentrated among a few key players that dominate global output. Based on production volume, revenue, and market influence, the following list highlights the top 8 largest steel manufacturing companies shaping the industry’s landscape and driving innovation amid evolving environmental and technological challenges.

Top 8 Largest Steel Companies Manufacturers 2026

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Largest Steel Companies

H2: 2026 Market Trends for the Largest Steel Companies

As the global economy evolves amid technological advancements, decarbonization pressures, and shifting geopolitical dynamics, the largest steel companies are poised to navigate a complex and transformative landscape by 2026. This analysis explores key market trends shaping the industry, focusing on sustainability, digitalization, consolidation, raw material volatility, and regional demand shifts.

-

Accelerated Decarbonization and Green Steel Initiatives

By 2026, environmental, social, and governance (ESG) compliance will be a decisive factor for steelmakers. The European Union’s Carbon Border Adjustment Mechanism (CBAM) and similar policies in North America and Asia are pushing major producers like ArcelorMittal, Nippon Steel, and Baowu Steel Group to accelerate green steel production. Hydrogen-based direct reduced iron (DRI) and electric arc furnace (EAF) technologies are expected to gain traction, with companies investing heavily in pilot plants and commercial-scale low-carbon facilities. Baowu Steel, for instance, aims to achieve carbon neutrality by 2050 and has already launched hydrogen-based steel projects, positioning itself as a leader in green innovation. -

Digital Transformation and Smart Manufacturing

The integration of artificial intelligence (AI), Internet of Things (IoT), and advanced analytics into steel production is expected to mature by 2026. Leading companies are deploying digital twins and predictive maintenance systems to optimize energy use, improve yield rates, and reduce downtime. Tata Steel and POSCO are among those investing in smart factory ecosystems that enhance operational efficiency and product quality. This technological shift not only improves margins but also enables faster response to market fluctuations and customer-specific demands. -

Consolidation and Strategic Alliances

Market pressures and the need for scale in green transition are driving consolidation. By 2026, we anticipate further mergers, acquisitions, and cross-border partnerships among top steel firms. For example, the proposed merger between JSW Steel and Tata Steel’s India operations could create one of the world’s largest steel producers, enhancing competitive positioning in Asia and global markets. Additionally, joint ventures focused on green steel—such as those between European and Middle Eastern firms—are likely to increase, combining capital, technology, and low-carbon energy sources. -

Volatility in Raw Material Supply Chains

Iron ore and coking coal prices are expected to remain volatile due to geopolitical tensions, mining constraints, and ESG-driven supply restrictions. By 2026, steel giants will increasingly secure long-term contracts with diversified suppliers and explore alternative materials such as recycled steel and scrap. The rise of circular economy models is pushing companies like Nucor and Steel Dynamics to expand their scrap-based EAF capacities, reducing dependency on virgin raw materials and improving sustainability metrics. -

Shifts in Regional Demand Dynamics

China’s steel demand is projected to plateau or decline slightly by 2026 as infrastructure and real estate growth slows. In contrast, India, Southeast Asia, and parts of Africa are expected to emerge as key growth markets due to urbanization and infrastructure development. Major steel companies are expanding their footprint in these regions through greenfield investments or joint ventures. For instance, ArcelorMittal is increasing its stake in Indian operations, while Hyundai Steel targets Southeast Asia for export growth. -

Trade Policies and Geopolitical Risks

Protectionist trade measures, anti-dumping duties, and supply chain localization efforts will continue to influence market access. The U.S. Inflation Reduction Act (IRA) and EU Green Deal are incentivizing domestic production of low-carbon steel, potentially reshaping global trade flows. By 2026, the largest steel companies will need to adapt by localizing production, complying with regional standards, and managing tariff-related risks.

Conclusion

By 2026, the world’s largest steel companies will be operating in a fundamentally transformed industry. Success will hinge on strategic investments in decarbonization, digital innovation, and global market positioning. Companies that proactively embrace sustainability, agility, and collaboration are likely to lead the next era of steel production, turning regulatory and environmental challenges into competitive advantages.

Common Pitfalls When Sourcing from the Largest Steel Companies (Quality, IP)

Sourcing from the world’s largest steel producers can offer advantages like scale, advanced technology, and global reach. However, it also presents significant risks related to quality consistency and intellectual property (IP) protection. Being aware of these common pitfalls is essential for mitigating supply chain vulnerabilities.

Overlooking Regional Quality Variability

Even within the largest steel companies, production facilities may be spread across multiple countries with varying quality standards, oversight, and operational practices. A mill in one region may adhere to strict international standards (e.g., ISO, ASTM), while another under the same corporate umbrella may prioritize cost-efficiency over consistency. Buyers often assume uniform quality across all facilities, leading to unexpected defects or non-compliance in delivered materials.

Neglecting Certification and Traceability Verification

Large steel producers may provide extensive documentation, but this does not guarantee authenticity or traceability. Counterfeit certifications or lapses in material test reports (MTRs) can go unnoticed without rigorous third-party verification. Relying solely on supplier-provided paperwork increases the risk of receiving substandard or misrepresented steel, especially in high-performance applications like aerospace or energy.

Underestimating Intellectual Property Risks in Custom Alloys

When sourcing proprietary or custom-engineered steel grades, there is a significant risk of IP exposure. Major steel companies may claim ownership over process innovations or alloy compositions developed jointly with clients. Without clear contractual agreements defining IP ownership, confidentiality, and usage rights, buyers may lose control over critical design elements or face restrictions on sourcing alternatives.

Assuming Scale Equals Reliability

The size and global reputation of a steel producer can create a false sense of security. Large companies may prioritize high-volume contracts or strategic accounts, leading to delayed responses, reduced flexibility, or deprioritization of smaller or technically complex orders. This can result in supply chain disruptions or compromise in tailored quality requirements.

Inadequate Oversight of Subcontracted Production

To meet demand, large steel companies may subcontract part of the production or finishing processes to third-party mills or service centers. These subcontractors may not adhere to the same quality protocols or IP safeguards, increasing the risk of contamination, dimensional inaccuracies, or unauthorized technology transfer. Without visibility into secondary supply chains, buyers face hidden vulnerabilities.

Failing to Enforce Audit and Compliance Clauses

Many procurement contracts with large suppliers lack enforceable audit rights or real-time quality monitoring provisions. Without the ability to conduct unannounced facility audits or require real-time data sharing (e.g., melt chemistry, heat treatment logs), buyers are often reactive rather than proactive in addressing quality deviations or IP breaches.

Overreliance on Long-Term Contracts Without Performance Metrics

Long-term agreements with major steel suppliers are common but can become problematic if they lack clear performance metrics tied to quality consistency, delivery accuracy, and IP protection. Without periodic reviews and exit clauses, companies may remain locked into unfavorable terms even when standards deteriorate or IP concerns arise.

Logistics & Compliance Guide for the Largest Steel Companies

The global steel industry operates within a complex web of logistics challenges and stringent regulatory requirements. For the largest steel producers, efficient logistics and robust compliance are not just operational necessities—they are strategic imperatives that impact cost, competitiveness, environmental performance, and market access. This guide outlines key considerations for managing logistics and compliance at scale.

Strategic Logistics Management

Global Supply Chain Network Design

Largest steel companies must optimize a multi-tiered supply chain spanning raw material sourcing (iron ore, coal, scrap), production facilities, distribution centers, and end customers. Strategic network design involves:

– Locating production plants near raw material sources or major markets to minimize transportation costs.

– Establishing regional distribution hubs to improve delivery times and responsiveness.

– Utilizing port-adjacent facilities for efficient import/export operations.

Multimodal Transportation Optimization

Steel products are heavy and bulky, requiring cost-effective and reliable transport solutions:

– Rail: Ideal for long-distance bulk movement of raw materials and finished products.

– Maritime: Essential for international trade; requires coordination with shipping lines and port authorities.

– Trucking: Critical for last-mile delivery and flexible scheduling.

– Inland waterways: Used where available for lower-cost transport.

Leveraging intermodal solutions reduces costs and environmental impact.

Inventory & Warehouse Management

Effective inventory control balances supply-demand fluctuations:

– Just-in-time (JIT) inventory models reduce holding costs while ensuring supply continuity.

– Digital twin technologies and warehouse management systems (WMS) enhance visibility and efficiency.

– Segmentation of high-value or specialized steel products (e.g., automotive-grade) requires dedicated storage and handling.

Digitalization & Supply Chain Visibility

Advanced technologies enable real-time tracking and predictive analytics:

– IoT sensors monitor cargo conditions (e.g., temperature, humidity) during transit.

– Blockchain improves traceability of raw materials, supporting sustainability claims.

– AI-driven demand forecasting improves production and logistics planning.

Regulatory & Environmental Compliance

International Trade Regulations

Steel is one of the most regulated commodities globally:

– Anti-dumping and countervailing duties: Monitor trade policies across key markets (e.g., U.S., EU, India).

– Export controls: Comply with sanctions and dual-use regulations, especially for high-strength alloys.

– Customs compliance: Ensure accurate HS code classification, documentation (e.g., certificates of origin), and tariff management.

Environmental, Social, and Governance (ESG) Requirements

Investors and regulators demand transparency in sustainability practices:

– Carbon reporting: Comply with frameworks like EU ETS, CBAM (Carbon Border Adjustment Mechanism), and SEC climate disclosures.

– Scope 3 emissions tracking: Measure and reduce emissions across the value chain, including logistics.

– Circular economy initiatives: Promote scrap recycling and design for recyclability.

Health, Safety, and Environmental (HSE) Standards

Operational compliance is critical across global facilities:

– Adhere to OSHA (U.S.), COSHH (UK), and local safety regulations.

– Implement process safety management (PSM) for handling hazardous materials.

– Meet air and water emission standards (e.g., particulate matter, SOx, NOx).

Product Standards & Certification

Steel products must meet regional and industry-specific quality benchmarks:

– ASTM, ISO, EN standards for material properties and testing.

– API, ASME, or CE marking for industrial and structural applications.

– Automotive and aerospace certifications (e.g., IATF 16949) requiring rigorous quality control.

Risk Management & Resilience

Geopolitical & Market Risk Mitigation

Global steel companies face volatility from trade wars, sanctions, and supply disruptions:

– Diversify sourcing and customer base to reduce dependency on single markets.

– Monitor geopolitical developments and adjust logistics routes accordingly.

– Maintain contingency plans for supply chain disruptions.

Cybersecurity in Logistics Systems

As operations become more digital, protecting data is crucial:

– Secure transportation management systems (TMS), ERP, and IoT platforms.

– Conduct regular audits and employee training to prevent breaches.

Crisis Response Planning

Prepare for disruptions such as natural disasters, port closures, or labor strikes:

– Develop business continuity plans with alternative logistics providers.

– Maintain buffer stocks of critical materials where feasible.

Conclusion

For the largest steel companies, mastering logistics and compliance is a continuous process of adaptation and innovation. By integrating advanced technologies, adhering to evolving regulations, and building resilient supply chains, industry leaders can maintain operational excellence, reduce risk, and support sustainable growth in a highly competitive global market.

In conclusion, sourcing from the largest steel companies offers numerous advantages, including access to high-quality materials, consistent supply chain reliability, advanced manufacturing capabilities, and competitive pricing due to economies of scale. These industry leaders often comply with international standards and sustainability practices, making them ideal partners for large-scale construction, infrastructure, automotive, and manufacturing projects. However, thorough due diligence is essential to evaluate factors such as geographic proximity, lead times, customization options, and environmental commitments. By strategically partnering with top global steel producers, businesses can enhance operational efficiency, ensure material integrity, and support long-term growth in a competitive market.