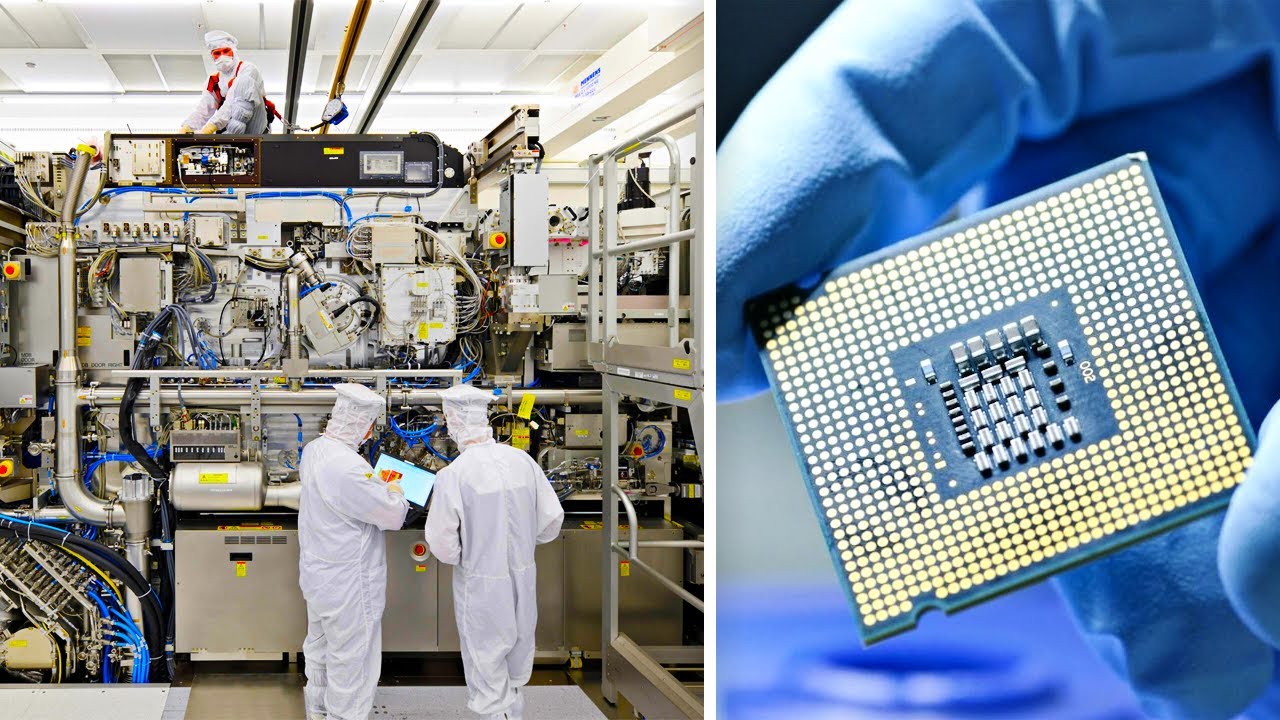

The global semiconductor industry is undergoing rapid transformation, driven by escalating demand across consumer electronics, automotive, artificial intelligence, and 5G infrastructure. According to a 2023 report by Mordor Intelligence, the semiconductor market is projected to grow at a CAGR of over 8.7% from 2023 to 2028, reaching a valuation of approximately USD 700 billion by the end of the forecast period. This expansion is underpinned by rising investments in chip fabrication, geopolitical shifts in supply chains, and increasing adoption of advanced process nodes. As innovation accelerates and demand outpaces supply in key regions, a select group of chip-making manufacturers are leading the charge in capacity, technology, and market share. These top ten companies not only dominate global wafer production but also set the pace for next-generation semiconductor development.

Top 10 Chip Making Companies Manufacturers 2026

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Chip Making Companies

2026 Market Trends for Chip Making Companies

The global semiconductor landscape is poised for transformative shifts by 2026, driven by technological innovation, geopolitical dynamics, and surging demand across key industries. Chip making companies, or semiconductor foundries and integrated device manufacturers (IDMs), will navigate a complex environment defined by advanced technology adoption, supply chain restructuring, and intensified competition.

Accelerated Adoption of Advanced Nodes and Packaging

By 2026, leading-edge process nodes—specifically 2nm and the initial commercialization of 1.4nm—will be critical battlegrounds for foundries like TSMC, Samsung, and Intel Foundry. Demand for high-performance computing (HPC), artificial intelligence (AI) accelerators, and next-generation mobile SoCs will compel fabless companies (e.g., NVIDIA, Apple, AMD) to push design starts into these nodes. Concurrently, advanced packaging technologies—such as Chiplets, 3D stacking (e.g., SoIC, Foveros), and Co-Packaged Optics—will move from niche to mainstream. This shift enables heterogeneous integration, improving performance and power efficiency without relying solely on process scaling, and presents new revenue opportunities for foundries offering integrated design and packaging services.

Geopolitical Fragmentation and Regionalization of Supply Chains

The trend toward regional self-sufficiency in semiconductor manufacturing, catalyzed by U.S. CHIPS Act, EU Chips Act, and similar initiatives in Japan, India, and China, will mature by 2026. Foundries will operate under a “China +1” or “multi-polar” manufacturing strategy, with expanded fab capacity in the U.S. (Arizona, Ohio), Europe (Germany, France), and Southeast Asia. While this diversification reduces supply chain risk, it increases capital expenditures and operational complexity. Export controls and technology restrictions—particularly on EUV lithography tools and AI-related chips—will continue to shape R&D priorities and market access, especially for Chinese semiconductor firms.

AI-Driven Demand and Specialized Compute Architectures

Artificial intelligence remains the dominant growth vector for semiconductors in 2026. Demand for AI training chips, inference accelerators, and data center GPUs will sustain high utilization rates at advanced-node foundries. This will incentivize investments in specialized process optimizations—for example, enhanced SRAM density, high-bandwidth memory (HBM) integration, and low-power logic for edge AI. Foundries that can offer AI-optimized process design kits (PDKs) and co-development partnerships will gain competitive advantage. Additionally, AI will increasingly be embedded into chip design and manufacturing workflows via generative design and predictive yield management.

Maturation of Specialty and Mature Node Markets

While headlines focus on cutting-edge nodes, mature and specialty process nodes (28nm and above) will remain vital in 2026. The automotive, industrial IoT, and consumer electronics sectors continue to rely on RF, power management, analog, and MEMS chips fabricated on these nodes. Foundries like UMC, SMIC, and GlobalFoundries will benefit from stable demand and higher margins in these segments. Additionally, geopolitical diversification efforts will support investment in mature-node capacity to ensure resilience in supply chains for mission-critical applications.

Capital Intensity and Sustainability Challenges

The escalating cost of building and operating leading-edge fabs—exceeding $20 billion per facility—will place immense pressure on foundry economics. By 2026, only a handful of companies will sustain investments in sub-2nm nodes, potentially consolidating market leadership. At the same time, environmental, social, and governance (ESG) concerns will grow, with increasing scrutiny on water usage, energy consumption, and chemical waste in semiconductor manufacturing. Foundries will need to demonstrate progress in sustainable practices, including renewable energy adoption and closed-loop water systems, to meet regulatory and customer demands.

In conclusion, chip making companies in 2026 will operate in a highly stratified and geopolitically charged environment. Success will depend on strategic positioning across technology nodes, agility in adapting to regional policies, and the ability to deliver integrated solutions that meet the performance and efficiency demands of AI and next-generation computing.

Common Pitfalls When Sourcing Chip Making Companies (Quality, IP)

Sourcing semiconductor manufacturing partners involves significant technical, financial, and strategic risks. Two of the most critical areas where companies encounter pitfalls are quality assurance and intellectual property (IP) protection. Failing to address these properly can lead to product failures, legal disputes, and reputational damage.

Quality-Related Pitfalls

Inadequate Process Control and Yield Management

Many sourcing teams underestimate the importance of a foundry’s process control capabilities. Poor process consistency leads to low yields and unreliable chips. It’s essential to evaluate a manufacturer’s statistical process control (SPC) systems, defect density metrics (e.g., D0), and historical yield data for similar process nodes.

Lack of Certification and Compliance

Choosing a chip maker without proper industry certifications—such as ISO 9001, IATF 16949 (for automotive), or AEC-Q100 qualification—can result in non-compliant products. These certifications ensure adherence to quality management systems and reliability standards critical for high-stakes applications.

Insufficient Testing and Validation Protocols

Some manufacturers offer limited or opaque testing procedures. Relying on incomplete wafer probe testing, burn-in processes, or lack of comprehensive reliability testing (e.g., HTOL, ESD, latch-up) increases the risk of field failures. Ensure the foundry provides detailed test coverage and supports custom test programs.

Overlooking Supply Chain Traceability

Poor material traceability and lack of control over raw materials (e.g., silicon wafers, chemicals) can introduce quality inconsistencies. Verify that the manufacturer maintains a transparent supply chain and uses qualified material suppliers.

Intellectual Property (IP)-Related Pitfalls

Weak IP Protection Agreements

Many companies assume that standard NDAs are sufficient to protect their designs. However, without robust IP clauses in manufacturing contracts—including clear ownership definitions, reverse engineering prohibitions, and audit rights—there’s a risk of IP leakage or unauthorized use.

Foundry Access to Sensitive Design Data

When outsourcing fabrication, design files (GDSII, netlists) are shared with the manufacturer. Without secure data transfer protocols and access controls, there’s a risk of design theft or duplication. Ensure the foundry employs secure data handling practices and restricts access to authorized personnel only.

Third-Party IP Infringement Risks

Some chip makers use third-party IP blocks (e.g., standard cells, I/O libraries) in their process design kits (PDKs). If these blocks are improperly licensed, your final product could infringe on patents. Require indemnification clauses and documentation of IP provenance from the foundry.

Geopolitical and Jurisdictional Risks

Manufacturing in certain regions may expose IP to legal frameworks with weak enforcement or state-sponsored surveillance. Evaluate the geopolitical landscape and legal environment of the foundry’s location, especially concerning data sovereignty and export controls (e.g., U.S. EAR, China’s cybersecurity laws).

Avoiding these pitfalls requires thorough due diligence, legal safeguards, and ongoing oversight. Partnering with reputable, transparent chip makers—and engaging legal and technical experts in the selection process—is essential to protect both product quality and intellectual property.

Logistics & Compliance Guide for Chip Making Companies

The semiconductor manufacturing industry operates in a highly complex, globalized environment where precision, speed, and regulatory adherence are critical. Chip making companies must manage intricate supply chains, sensitive materials, and a dense web of international regulations. This guide outlines essential logistics and compliance considerations to ensure operational resilience, legal compliance, and competitive advantage.

Supply Chain Management & Logistics

Effective logistics is the backbone of semiconductor manufacturing. Delays or disruptions can result in significant financial losses due to the high value and time-sensitive nature of production.

Establish Resilient Supply Chains

Develop a multi-sourced supplier strategy to mitigate risks from geopolitical instability, natural disasters, or trade restrictions. Map your entire supply chain, including sub-tier suppliers, to identify single points of failure. Implement dual- or multi-sourcing for critical materials such as specialty gases, photoresists, and silicon wafers.

Implement Just-in-Time and Just-in-Case Hybrid Models

While just-in-time (JIT) delivery helps reduce inventory costs, chip manufacturers should maintain strategic stockpiles of critical components and raw materials (just-in-case). This hybrid approach balances efficiency with risk mitigation, particularly in light of recent global supply chain disruptions.

Optimize Transportation of Sensitive Materials

Semiconductor materials often require strict environmental controls (e.g., temperature, humidity, static protection). Use certified carriers with experience in handling high-value, contamination-sensitive cargo. Employ real-time tracking, shock sensors, and tamper-evident packaging to ensure integrity during transit.

Manage Cross-Border Logistics Efficiently

Leverage free trade zones (FTZs) and bonded warehouses to defer customs duties and streamline international movement. Pre-classify goods under Harmonized System (HS) codes and maintain accurate documentation to avoid customs delays. Consider nearshoring or regionalization strategies to reduce transit times and exposure to tariffs.

Regulatory Compliance

Compliance with international, national, and industry-specific regulations is non-negotiable in semiconductor manufacturing. Non-compliance can result in fines, shipment delays, or loss of market access.

Adhere to Export Control Regulations

Semiconductor technology is subject to strict export controls due to its strategic importance. Key frameworks include:

– U.S. Export Administration Regulations (EAR) – Administered by the Bureau of Industry and Security (BIS), EAR controls the export of dual-use items, including advanced chips and fabrication equipment.

– Wassenaar Arrangement – A multilateral export control regime that includes controls on semiconductor manufacturing equipment and related technologies.

– Foreign Direct Product Rule (FDPR) – Extends U.S. export controls to foreign-made products using U.S. technology or software.

Conduct regular classification reviews of products and technologies. Implement internal compliance programs (ICPs) that include screening of customers, partners, and destinations against restricted party lists (e.g., U.S. OFAC, EU Consolidated List).

Ensure Environmental, Health, and Safety (EHS) Compliance

Chip fabrication involves hazardous chemicals and high-energy processes. Compliance with EHS standards is mandatory:

– OSHA (U.S.) / REACH and CLP (EU) – For handling, labeling, and disposal of hazardous substances.

– Clean Air Act and Clean Water Act (U.S.) – For emissions and wastewater management.

– RoHS and WEEE Directives (EU) – For restricting hazardous substances and managing end-of-life electronics.

Maintain up-to-date Safety Data Sheets (SDS), train employees regularly, and conduct internal audits to ensure adherence.

Meet International Trade and Customs Requirements

Accurate documentation, proper valuation, and correct origin determination are essential for smooth customs clearance. Utilize Authorized Economic Operator (AEO) status where available to benefit from expedited processing. Ensure compliance with:

– Customs-Trade Partnership Against Terrorism (C-TPAT) – For shipments to the U.S.

– Import Control System 2 (ICS2) – For EU-bound shipments, requiring advance electronic data submission.

Manage Intellectual Property (IP) and Technology Transfer Risks

Protect proprietary processes and designs through robust IP strategies. Limit technology transfer through controlled access, non-disclosure agreements (NDAs), and compliance with licensing requirements. Monitor joint ventures and foreign collaborations for unauthorized dissemination of sensitive know-how.

Cybersecurity and Data Compliance

Semiconductor companies handle vast amounts of sensitive data, from design blueprints to customer information. Cybersecurity is integral to both logistics and compliance.

Secure Supply Chain Data Flows

Use encrypted communication channels for data exchange with suppliers and logistics partners. Implement cybersecurity standards such as ISO/IEC 27001 and NIST Cybersecurity Framework. Conduct regular third-party risk assessments.

Comply with Data Privacy Laws

Adhere to data protection regulations such as:

– General Data Protection Regulation (GDPR) – For handling personal data of EU residents.

– California Consumer Privacy Act (CCPA) – For data of California residents.

– China’s Personal Information Protection Law (PIPL) – For operations in China.

Ensure lawful data transfers across borders, especially when cloud services or global teams are involved.

Sustainability and ESG Reporting

Environmental, Social, and Governance (ESG) performance is increasingly scrutinized by regulators, investors, and customers.

Reduce Carbon Footprint in Logistics

Optimize routing, consolidate shipments, and use low-emission transport modes where possible. Report logistics-related emissions under frameworks such as the Greenhouse Gas (GHG) Protocol.

Comply with Conflict Minerals and Responsible Sourcing Rules

Under U.S. SEC Rule 13p-1 and EU Conflict Minerals Regulation, companies must disclose the use of tin, tantalum, tungsten, and gold (3TG) sourced from conflict-affected areas. Conduct supply chain due diligence and use validated sourcing programs like the Responsible Minerals Initiative (RMI).

Report ESG Metrics Transparently

Disclose energy usage, water consumption, waste management, and supply chain labor practices in annual sustainability reports. Align with standards such as GRI, SASB, and TCFD to enhance credibility.

Conclusion

For chip making companies, mastering logistics and compliance is not merely a regulatory obligation—it is a strategic imperative. By building resilient supply chains, adhering to export and environmental regulations, securing data, and embracing sustainability, semiconductor manufacturers can navigate global complexities while safeguarding innovation and market access. Continuous monitoring, employee training, and investment in compliance technology are essential to stay ahead in this high-stakes industry.

In conclusion, sourcing semiconductor (chip) manufacturing companies requires a strategic and well-informed approach due to the complexity, capital intensity, and technological sophistication of the industry. Key considerations include evaluating a manufacturer’s process node capabilities, production capacity, geographic location, supply chain resilience, and compliance with international regulations and quality standards. Leading foundries such as TSMC, Samsung Foundry, and Intel Foundry offer cutting-edge technology but may have limited availability and higher costs, while other regional players like GlobalFoundries, SMIC, and UMC provide viable alternatives for mature nodes or specific regional needs.

Building strong partnerships, ensuring long-term contracts, and diversifying the supplier base can mitigate risks associated with geopolitical tensions, supply chain disruptions, and surging demand. Additionally, staying abreast of government incentives—such as those under the U.S. CHIPS Act or the EU’s semiconductor initiatives—can inform sourcing decisions and reduce dependency on a single region.

Ultimately, successful sourcing in the chip manufacturing sector hinges on aligning technical requirements with business goals, fostering transparent collaboration with suppliers, and maintaining agility in a rapidly evolving global landscape.